How to Find the Right Debt Consolidation Loan Option

In Canada there are now eight commonly used ways to consolidate debt. Each debt consolidation option has distinctive pros and cons and not every option is a available to everyone. It all depends on your situation. Below you can learn more about each of these options to get a better feel for which option may be right for you. We also discuss the types of debt consolidation companies and organizations that offer these various options. If this is too much information for you, just skip to the end where we tell you who you can sit down with to discuss these options and get some free advice.

Overview of Canada's 8 Debt Consolidation Options

- Consolidate using a Debt Consolidation Loan

- Consolidate using a Home Equity Loan / Refinance Mortgage / Second Mortgage

- Consolidate using a Line of Credit or Overdraft

- Consolidate debt on your Credit Cards

- Consolidate using a Debt Management Program

- Consolidate by doing a Debt Settlement

- File a Consumer Proposal

- Consolidate by Borrowing from Family or Friends

How to Get Good Debt Consolidation Advice for Free

1. Consolidate using a Debt Consolidation Loan

A debt consolidation loan is where a bank, credit union or finance company provides you with the money to pay off your outstanding debts and "consolidate" them (bring them all together) into one big loan. This usually provides you with three advantages:

Advantages of a Debt Consolidation Loan

- You only have one monthly payment to worry about

- You often consolidate at a lower interest rate which saves you money

- Your debt will be paid off in a set amount of time (typically 2 - 5 years)

- Any fees charged for this service are usually very low

Debt Consolidation Loan Interest Rates

Banks and credit unions usually offer the best interest rates for debt consolidation loans. Many factors can help you get a better interest rate with a bank or credit union including your credit score, your net worth, whether or not you have a relationship with them and whether or not you can offer good security (collateral) for a loan. Good security for a debt consolidation loan will often be a newer model vehicle, boat, term deposit (non-RRSP) or another asset that can easily be sold or liquidated by the bank if you don't pay make your loan payments.

For the past decade, banks have typically charged interest rates on debt consolidation loans of around 7% - 12%. Finance companies tend to charge anywhere from 14% for secured loans to over 30% for unsecured loans.

Disadvantages of a Debt Consolidation Loan

- They usually require security (collateral)

- You must have a decent credit score

- Interest rates are higher than a home equity loan (refinancing your home)

- Interest rates for unsecured debt consolidation loans can be high

While banks rarely approve unsecured debt consolidation loans, some do get approved from time to time. To qualify for one of these you would typically need to have a high net worth (the value of your assets after you subtract all of your debts) and a very strong credit score or a co-signer who has a very high net worth and a very strong credit score.

What are your chances of getting a Debt Consolidation Loan?

If your credit score meets the bank's minimum requirement (meaning: not too many late payments or any big negatives on your credit report), you earn enough income, your total monthly minimum debt payments aren't too high and you can offer some good security for a loan, then you may qualify for a debt consolidation loan. If you don't quite meet all of these requirements on your own, you may still be able to qualify if you can find a good co-signer.

If your minimum monthly debt payments are too high--even after a consolidation loan is factored into the situation, you have bad credit, or you can't offer some reasonable security for a loan, then a consolidation loan probably won't work. If this is the situation that you are in, then check out some of the other options below to see if something else might work. However, if you don't qualify for a debt consolidation loan, then a solution to your situation may be a little more complex than you may have thought and your best bet may be to speak with an experienced Credit Counsellor as soon as possible so that you can find the right solution before it's too late. Speaking with a non-profit Credit Counselor is completely free and most of them possess a tremendous amount of experience in the credit industry. No matter how complicated your situation may be, they should be able to help you figure out the right solution.

2. Consolidate using a Home Equity Loan / Refinance Mortgage / Second Mortgage

A "Home Equity Loan", "Refinancing your Mortgage" and getting a "Second Mortgage" are all different names for the same thing. These terms refer to the bank lending you money against the portion of your home that you own. So if the bank thinks that your home is worth $300,000 and your mortgage is for $250,000, then you own $50,000 of your house. This is called your "equity". The bank may let you take out a second mortgage to use up some of this equity to pay off your debts. You would then have two mortgages: your first mortgage and a second mortgage which could be your debt consolidation loan. There is a lot more to this process than we've mentioned here. So talk to your bank or credit union if you would like to learn more about this.

Interest Rates for Second Mortgages

Many times you can get the same interest rate on your second mortgage as you got on your first mortgage, but this isn't always possible (talk to your bank to find out more). If you do have to pay a higher interest rate on your second mortgage you can setup the due date for your second mortgage term to correspond with the due date for you first mortgage so that you can combine them together at the bank's best interest rate when they need to be renewed (again talk to your bank to learn more).

Ever since the early 1980's mortgage rates have been declining. They peaked at over 20% in the early eighties but are now typically offered in the 2% - 5% range. It is wise to remain mindful of the fact that these are historically low interest rates. This means that we cannot count on them to stay this low forever. The average five year mortgage rate over the past 60 years has been 8.95%. So if you are considering refinancing your home, make sure you can afford an "average" interest rate of 9% in the long term.

Finance companies and sub-prime lenders also offer mortgages. Their interest rates will almost always be higher than the bank's and can often range between 14% - 30%. These rates are a lot higher because these companies tend to lend money to people in financial situations that involve more risk than banks usually want to take on.

High interest loans like these can be used as a tool to get you from point A to point B, but you should do your best to find a better arrangement as fast as possible. It is very hard to get ahead paying really high interest rates.

Advantages of using a Second Mortgage to Consolidate Debt

- Typically very low interest rates

- Flexible payment arrangements. You can usually extend your amortization (the length of time required to pay back the loan) to create an ideal monthly payment

Disadvantages of a Second Mortgage

- You must have enough equity in your home

- You may be charged a number of fees for the costs involved in setting up a 2nd mortgage

- Banks often don't like to do small second mortgages. $10,000 may be the minimum that they will consider

3. Consolidate using a Line of Credit or Overdraft

Before the recession hit, it seemed as though banks were giving out lines of credit for $5,000 to $20,000 to almost everyone they could. Now that the global economy has changed, a line of credit may be much harder to qualify for. You can check with your bank or credit union to see what their criteria is. Usually they want you to have a very good credit score, a good income and hopefully a good, positive net worth (but this isn't always necessary).

Lines of credit and overdrafts can be secured or unsecured. It depends on your situation and the bank's lending policy at the time (lending policy changes from time to time depending on the perceived health of the economy).

A line of credit and an overdraft are essentially the same thing. They both turn your bank card (debt card) into a credit card so you can spend money you don't have up to a predetermined limit. Just like a credit card, you only have to make a minimum payment each month.

Interest Rates for a Line of Credit or Overdraft

An overdraft is usually the expensive form of a line of credit. Banks and credit unions can charge over 20% interest (just like a credit card) plus a monthly fee. Lines of credit on the other had are priced based on the Prime interest rate that the Bank of Canada sets. Your interest rate then "floats" with the Prime Rate. So your bank may give you a line of credit for something like Prime + 2%. If the prime rate is currently 1.5%, that would mean that you would pay 3.5% interest (1.5% Prime Rate + 2% added on by the bank). Because the Prime Rate has been so low in recent years, some people are paying as low as 1% on their lines of credit while others who have lower credit scores or a lower net worth may be paying as much as 8%.

Advantages of using a Line of Credit or Overdraft to Consolidate Debt

- Lines of credit can offer the lowest interest rates possible

- Their minimal monthly payments can provide great flexibility

- They can give you tremendous freedom. You can pay it off as fast or as slow as you want

Disadvantages of using a Line of Credit or Overdraft to Consolidate your Debt

- If you don't discipline yourself to pay a set amount each month that is a lot more than your minimum payment, your debt will never go away. For this reason a line of credit can be an unexpected trap for many people

- A line of credit's interest rate floats with the Bank of Canada prime rate. If the prime rate goes up substantially, your minimum payments may become unmanageable. It would be a mistake to think that this couldn't happen

- An overdraft's interest rate and monthly fee can make it more expensive than a credit card

4. Consolidate by using your Credit Cards

If you can't find a debt consolidation company who will provide you with a reasonable debt consolidation loan you could try to consolidated all of your credit card balances onto one low interest rate card and then aggressively pay off this card by paying a set amount each month that you determine in advance. For example, the minimum payment on the card may be $50, but if you choose to pay $500 every month, you will have the balance paid off in a reasonable amount of time.

From time to time credit cards offer very low promotional interest rates. Some people use these as an opportunity to consolidate their debts. This may work for a while, but the reason why credit cards offer these promotional rates is because most people don't pay off their balances in a timely fashion and end up getting stuck at a higher interest rate when the promotional interest rate expires.

Many credit card companies also offer low interest rate credit cards if you can qualify for one. However, many times people who desperately want them don't qualify because their credit score is not high enough or they have too much debt. If this is your situation there are other options below that may work for you.

Advantages of Consolidating with Credit Cards

- Low interest cards are available along with low promotional interest rates

- Having all your debt in one place can make it easier for you to keep track of what you owe and start paying it down

- Payment flexibility. You can pay much more than your minimum payment each month, but if an emergency arises you can temporarily fall back to your minimum payment

Disadvantages of Consolidating with Credit Cards

- Many people who need a consolidation loan don't qualify for low rate cards

- Promotional interest rates usually only last for a number of months

- Once a promotional rate ends, normal interest rates are typically very high

- If you don't create a budget, spend less than you earn, and discipline yourself to pay more than your minimum payment each month, you may take decades to pay off your debt using a credit card

5. Consolidate using a Debt Management Program

If none of the previously listed debt consolidation options work for you, then a Debt Management Program may be the right fit for your situation. A Debt Management Program consolidates all of your credit card payments into one monthly payment. You then make this one monthly payment to a credit counseling organization and they disperse all of the funds to your various creditors. Your creditors have to agree to allow you to go onto this program, but they typically will if a non-profit credit counselor believes that this program is the right fit for your situation and sends them a proposal that demonstrates this. If you enroll in a Debt Management Program all of your credit card debt will be paid off within 5 years. However, most people pay off their program as fast as they can and the average program is completed in under 3 years.

Interest Rates for Debt Management Programs

If you work with a reputable non-profit credit counseling organization your interest rates will typically be reduced to either zero or a very low interest rate (not all creditors go to zero, but most of the major ones do). For-profit credit counseling companies also try to help people by offering Debt Management Programs, but creditors often don't allow them to offer the same low interest rates that they allow non-profits to offer.

To cover their costs, non-profit credit counseling organizations usually charge small fees for their Debt Management Programs. For-profit companies typically charge a large upfront fee of thousands of dollars for this same service. Unfortunately, many times for-profit credit counseling agencies charge these large fees and then don't provide the same level of service. Reasons for this can include some creditors refusing to work with them, or refusing to allow their clients to receive the same drastically reduced interest rates that non-profit credit counseling services are allowed to offer.

Advantages of Consolidating with a Debt Management Program

- All credit card debt is often paid off in less than 3 years (5 years max)

- Low interest or no interest

- Your credit report and credit score can be completely repaired 2 years after you finish your debt management program

- Non-profits provide free one-on-one help, budgeting workshops and credit education

- This service can often provide dramatic intangible benefits like substantially lowering stress, helping people sleep again and improving family relationships that were strained by financial issues

Disadvantages of Consolidating with a Debt Management Program

- Not everyone can do it. Your creditors must agree with a Credit Counsellor that this program makes sense for your situation

- Impacts your credit score until 2 years after you finish your program

- For-profit credit counselling companies charge very large fees, but these can be safely avoided by working with a non-profit service

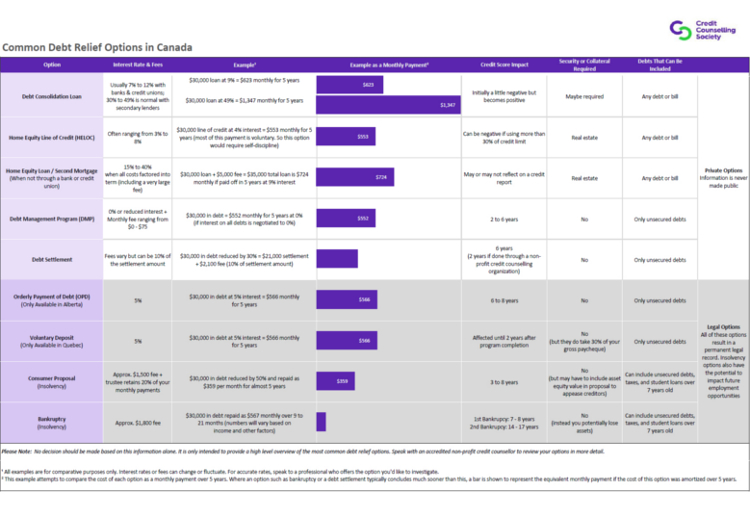

To learn more about a Debt Management Program or to speak with a non-profit Credit & Debt Counsellor to see if a program like this might be a good fit for your financial situation, click here to find a non-profit debt relief agency near you. You can also see all common debt relief options below and see how they compare to each other. This is only a high level overview. For more information, speak with a non-profit Credit Counsellor.

Click on the chart above to see a larger image. You can then zoom into the PDF that opens up.

6. Consolidate by doing a Debt Settlement

Up until October of 2010 Canadian debt settlements were primarily done in only one way. If you were having extreme difficulty paying your credit card debts and you happened to receive a large chunk of cash from somewhere, you could contact your creditors and offer to settle your debt with them for less than your full balance if they would accept a lump sum payment. If your creditor thought that this was a better option than waiting for you to completely pay them back, they might accept your offer and you might repay only 50% - 80% of your debt.

Anyone can call up their creditors and try to settle their debts in this manner but are unlikely to succeed. The most successful approach is to work with a credit counselling organization. They know what your creditors are likely to accept and what they won't even consider. Because most people don't have a rich uncle or a Fairy Godmother to lend them the money necessary to settle their debts, this isn't a realistic option for most people.

However, in October of 2010 Canada was introduced to a sensational new way of settling credit card debt that "could work for anyone"--or so the advertisements claimed. All you have to do is stop paying your creditors, save up your own money and then have an "expert negotiator" work out a settlement for you. Unfortunately, this method doesn't really work--even though American debt settlement companies spend millions of dollars advertising that it does work. After fielding thousands of complaints from angry US consumers and thoroughly investigating the matter, the US government enacted legislation in October 2010 to prevent for-profit US debt settlement companies from charging people fees for debt settlement services before providing a debt settlement service.

These American for-profit companies were charging people many different types of fees on a monthly basis for a service that 65% of their clients never received. The US Federal Trade Commission went on to discover that less than 10% of the people who signed up for these for-profit settlement programs successfully completed them, and rather than save their clients money as they so heavily advertise, they often costed many of their clients two to three times the amount of the debts that they settled. This is because it takes so long to save for a settlement that credit card interest, late fees and penalties often doubled or tripled the debt by the time it was settled.

To make matters worse for those who signed up for these programs, creditors would not stand by and wait while they skipped their monthly payments. They would naturally escalated their collections activities. This could include sending the debt to a collection agency, taking the client to court, seeking a judgment against the client and then garnishing the client's wages or putting a lien on their house.

Unfortunately, many of these US debt settlement companies are now advertising in Canada and are signing Canadians up for these disastrous for-profit programs that are now illegal in the United States.

Most Canadian non-profit credit counseling organization are very successful with negotiating debt settlements for the simple reason that they will not agree to negotiate unless the situation makes sense. All organizations charge a percentage of the settlement amount as a fee to pay for their service.

Interest Rates for doing a Debt Settlement

Once a creditor agrees to a settlement amount and you pay it by their settlement expiry date no more interest or fees are charged. The debt is then legally paid in full (as long as you have this in writing). Debt settlements can range from less than 20% to over 80%. It all depends on the situation. Someone who has become disabled and cannot work again or has suffered a debilitating illness would be an ideal candidate for a debt settlement. However, someone who is just trying to take advantage of their creditors doesn't stand a chance.

Advantages of using a Debt Settlement

- Potentially repay far less than you owe and quickly eliminate your debts

- Your credit can be completely repaired 2 years after your settlement is complete if you work with a non-profit organization

Disadvantages of using a Debt Settlement

- Need to have a lump sum of money available to settle. If you don't have a rich uncle or a Fairy Godmother, then this option is usually off the table

- For-profit debt settlement services have less than a 10% success rate and 65% of their clients do not receive any service in return for the fees that they pay according a US Federal Trade Commission study

- Your credit will be negatively impacted by a debt settlement. Your credit will take 6 - 7 years to recover if you work with a for-profit debt settlement company

7. File a Consumer Proposal

A Consumer Proposal is a legal process that can be used to deal with your debts when you don't qualify for a debt consolidation loan or a debt management program and you don't want to go bankrupt. Only Bankruptcy Trustees administer these programs. With a Consumer Proposal your Bankruptcy Trustee sends out a "proposal" to your creditors asking that they accept payment of less than the full amount of your debt. Creditors who hold at least half of your debts must agree to the proposal for it to work. If enough of your creditors don't agree to the proposal, you need to consider other options to deal with your debts. You may even need to file for bankruptcy. If enough of your creditors do accept the Bankruptcy Trustee's proposal, then you would have the opportunity to repay less than the full amount of your debt within 5 years. If you aren't able to consistently make your payments on this program, your proposal collapses and you aren't able to file another one. You may then need to file for bankruptcy.

Interest Rate for Consumer Proposal

Interest is completely stopped during this program.

Advantages of using a Consumer Proposal to deal with your debts

- No interest

- Repay less than you owe

- Last way to avoid bankruptcy

Disadvantages of using a Consumer Proposal

- If creditors holding at least half of your debt don't accept your proposal, you may need to look at other options

- It's a legal process. Once you start it, you cannot leave it

- Is reported on your credit report and negatively impacts your credit rating while you are on the program. This continues for 3 years after you've paid off the debt or 6 years from the date the proposal was filed, whichever comes first. A typical program lasts close to 5 years. So your credit may be effected for 6 years

- There are initial as well as ongoing fees to pay, along with your payments

- Over 20% recidivism rate - meaning 1 out of 5 people will need to repeat the program in the future

- Besides two legally mandated counselling sessions that occur in the first 6 months of the consumer proposal program, there is no one to help you learn money management skills or help you with your budget. This may be part of the reason for the high recidivism rate

8. Consolidate by Borrowing from Family or Friends

If you happen to have family or friends who are willing to lend you the money necessary to consolidate your debts, this can be a great option. However, if you ask a family member or friend for help, don't take offense if they turn you down. If they lend you the money you need and then unfortunate things happen which prevent you from paying them back, they are left with only two options:

- Forgive the debt and preserve their relationship with you, or

- Insist on repayment and lose their relationship with you

A friend or family member may value your relationship too much to jeopardize it by lending you money. Despite what you may think, they may not feel as though they can comfortably forgive your loan if things don't work out.

Regardless of everyone's best intentions, money can often come with strings attached, and even if it doesn't, in your mind you may begin to see the person differently who lent you the money if you find yourself struggling to make your payments.

While borrowing from family or friends may be a great option for some people to consolidate their debts, it may not be a wise move for others even if they have friends or relatives who are willing to lend the money.

How to Get Good Debt Consolidation Advice for Free

If all of these debt consolidation options seem a little overwhelming or if you just want to speak with an expert to find out what is best for your situation, there are two great places you can go and get some free advice.

Talk to your Bank or Credit Union about your Consolidation Options

If you don't know who your banker is just tell your bank or credit union that you would like to speak with someone about a debt consolidation loan. You can then fill out a loan application so that your banker can see what your financial situation looks like. They will then be able to let you know what they can do for you - and talking to your banker is completely free.

If your bank or credit union can't help you, don't worry. You may still have many options that your banker doesn't know about (a very large number of bankers only possess expertise about the products and services that banks sell. There are many options that some bankers are only vaguely familiar with because it's not part of their job). Your next stop should be to see a non-profit Credit Counsellor.

Talk to a Non Profit Credit Counsellor to discover all your Debt Consolidation Options

Finding out all of your options from reputable non profit Credit Counsellor can be worth its weight in gold. Many people become discouraged and feel hopeless when they find out that they can't get the debt consolidation loan that they feel they so desperately need. A Credit Counsellor can often help these people literally lift a huge weight from their shoulders as they realize that they do have options and they can again have hope for their future.

A non-profit Credit Counselor will quickly help you create a budget. They will then lay out all of your options for you based on your financial situation. You can then discuss the pros and cons of each option with the Counselor, and with their help you can figure out which options are in your best interest. Your Counselor will then help you create a plan to repay all of your debt and get your finances back on track so that you can get your debts behind you and begin working toward your goals and dreams.

If this sounds too good to be true, it's not. Credit Counsellors do this every day - usually for free. They are simply here to help. You can contact a non profit Counsellor to setup an appointment or to find out more.