Does It Make Sense to Accept a Limit Increase for Your Credit Card?

by Julie Jaggernath

Have you received an offer to raise the limit on your credit card? You know the ones, about how a lender wants to recognize your excellent credit history by giving you access to more credit. Are you wondering if it’s good to increase your credit card limit when offered?

It used to be that credit card companies could raise your limit without asking you, but the rules in Canada changed a while back for federally regulated financial institutions. Now, they need to get your permission first. In the past, I got a letter offering to raise my limit by more than double. While I was temporarily tempted to accept this credit limit increase, let me share a few details with you about why I quickly pushed all the paperwork through my shredder.

Increasing Credit Card Limits Can Lead to Temptation Spending

Increasing Credit Card Limits Can Lead to Temptation Spending

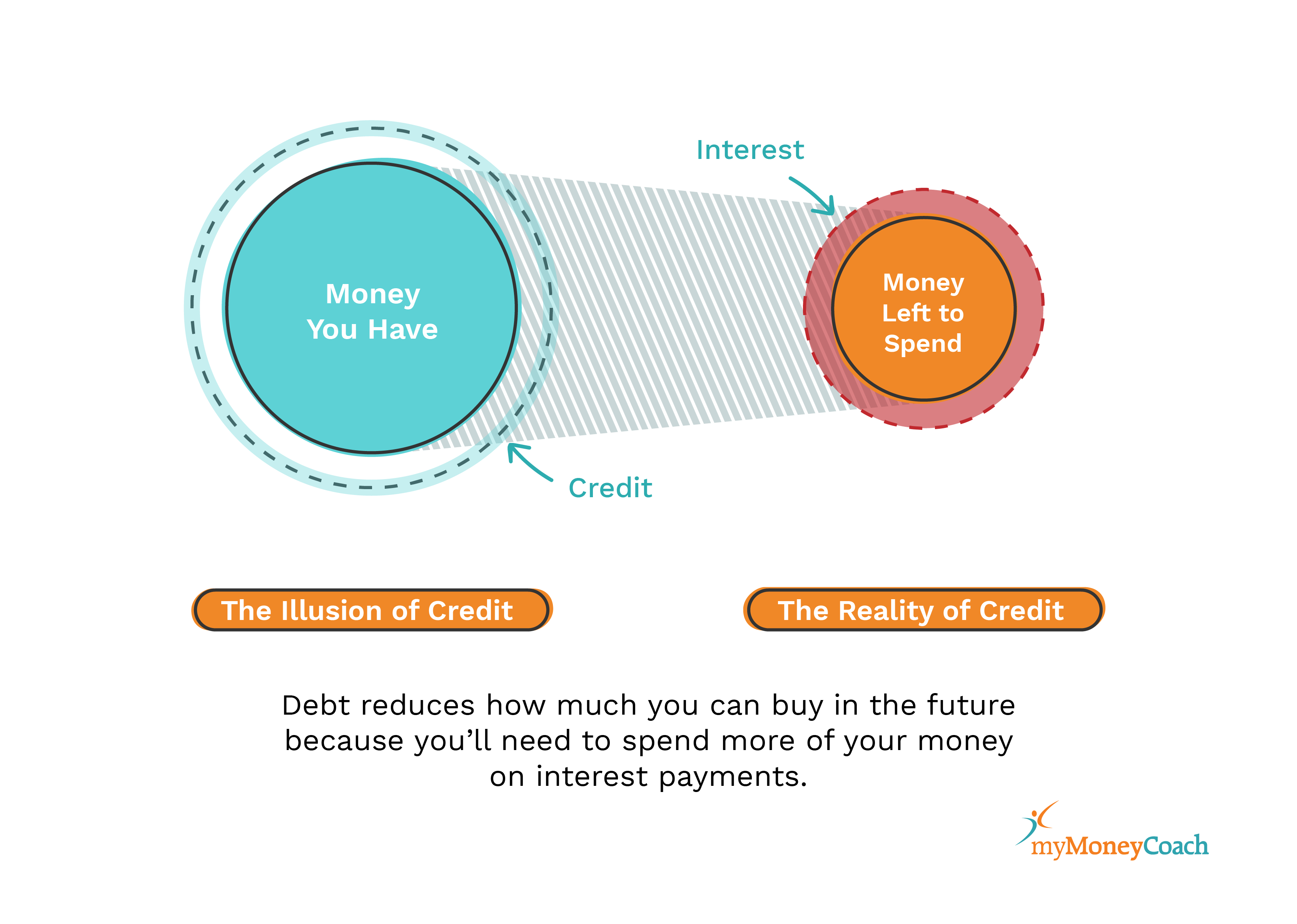

Increasing your credit card limits can make you feel richer than you really are and can even lead to impulse spending. This is a big disadvantage because it’s easy to spend more than you intended when you’re shopping with what seems like an endless amount of (someone else’s) money. However, it is also possible to use your credit card without getting into debt. In truth, the problem isn’t the credit card. It’s just a piece of plastic, so depending on how you use it, it’ll either be a flexible friend or foe.

High Credit Limits Impact Qualifying for a Car Loan, Personal Loan, Line of Credit, Debt Consolidation Loan or Mortgage

If you anticipate needing to borrow money in the next few years, keep the limits on your credit cards reasonable and in line with what your income allows you to repay. Higher limits on your existing credit accounts, even if you don’t fully utilize them, will limit how much you qualify for with any new or refinanced personal loan, debt consolidation loan, mortgage, car loan or line of credit. Even if you don’t anticipate borrowing any time soon, you should still be careful about requesting a credit limit increase. After all, no one ever really knows what life has in store for us, so it’s best to keep your financial house in order, just in case.

Raising Credit Card Limits Leaves More Opportunity for Fraud

Raising Credit Card Limits Leaves More Opportunity for Fraud

The credit card offer I received was for my “online” credit card, not for the credit card I use for in-person purchases. I have a separate credit card for online buying and I deliberately keep the credit limit low. If someone should get the number and use it fraudulently, at least I’m doing my part to try and minimize the damage. Of course, many Canadians do use the same card for both online and in-person purchases, both for convenience and to avoid needing to get new credit cards. If you’re one of them and need a higher credit limit for your planned and budgeted expenses, then take advantage of the ease in online banking to regularly check for unknown purchases.

Tips to Protect Your Money from Scams

How to Stop Credit Card Limit Increases

Thinking through the downsides to increasing your credit limit, especially when you don’t actually need that increase, helped me decide against it. As for how to stop it from happening – just ignoring the letter is fine, but you can also contact the company and ask them not to send any more offers to increase your limit. I did that because I’m not going to accept them anyways, so it saves me the time, energy, and potential temptation of getting more of them.

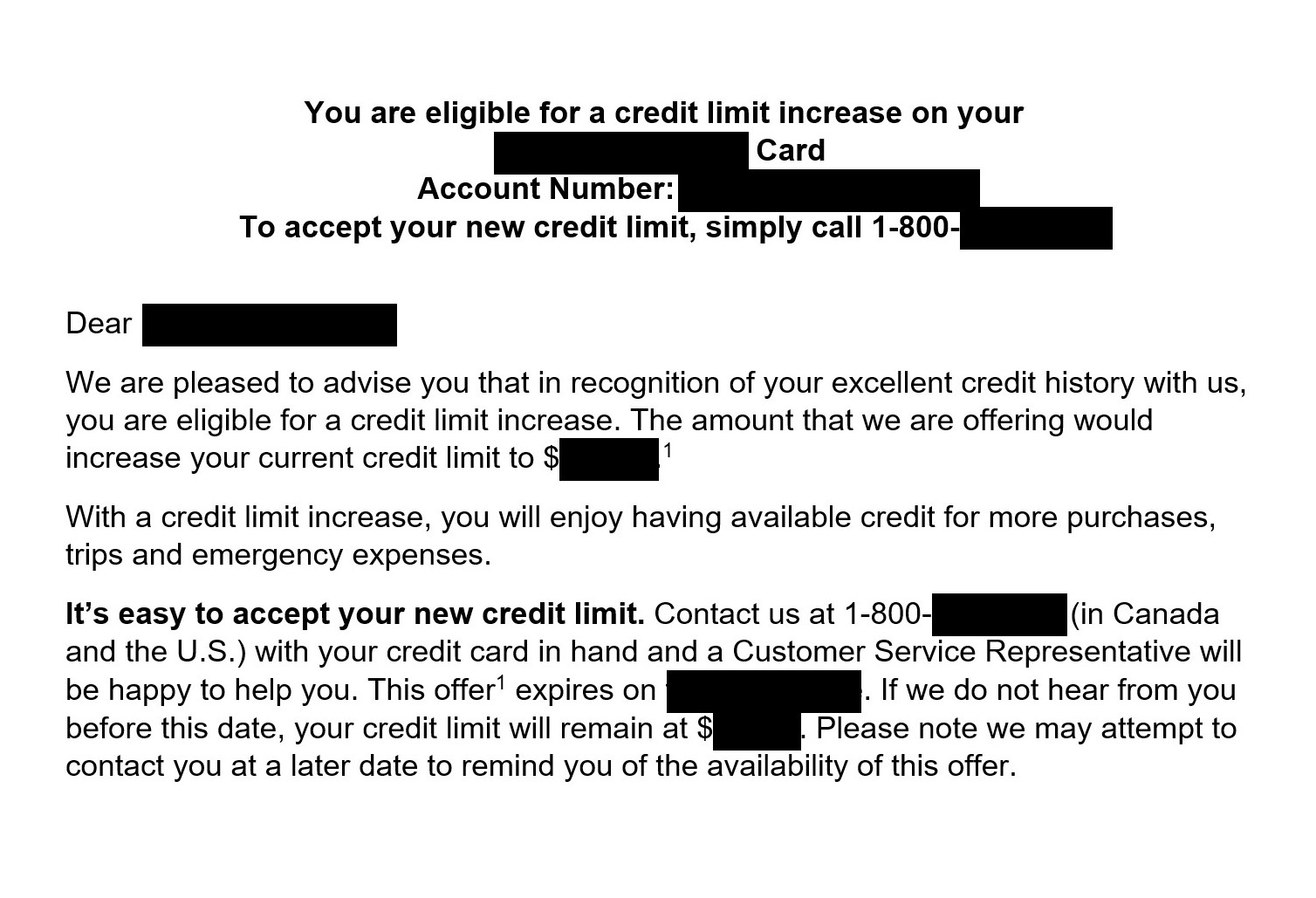

The above is an example of a credit card limit increase offer. Unless you really need the extra credit, and you won’t just be tempted to spend more, you might want to quickly push any letters you get through your shredder. An offer letter like this can lead to impulsive spending and debt that’s hard to repay.

The Benefits of Using a Credit Card

Just like with any tool, if you use a credit card wisely, there are benefits. For some people, they prefer to carry a credit card rather than cash, and others collect reward points with their credit card. When your budget allows you to pay your credit cards off in full every month, without incurring additional debt elsewhere, they can be a free, convenient way of managing money.

What to Do If You’re Worried About Your Credit Card Debt

If you’re one of the many Canadians who rely on their credit cards to make ends meet, take the time to understand the ins and outs of your card holder agreements. This will allow you to minimize your costs while you create a plan to manage your money better. Raising the limit on your credit card will not solve your debt problems, nor will using a low interest line of credit to pay off ongoing credit card debt. If you need help creating a budget and dealing with credit card debt and household bills, contact a non-profit credit counselling service for free guidance, information, and help to get back on track. Having a plan to deal with your money and debt troubles will ease your stress and worries. All you’ve got to lose is your debt!