What is a Credit Score & How is a Credit Score Calculated in Canada?

Do you wonder what a credit score is and how your credit score is calculated? Well wonder no more.

Here we’ll answer some of the questions we hear most often, including:

- What is a credit report?

- What is a credit score?

- What does a credit score mean?

- How is a credit score calculated in Canada?

- How can I find out what my credit score is?

- What can I do to improve my credit score?

What is a Credit Report?

A credit report is a summary of how you pay your financial obligations. It contains information based on what you have done in the past. Lenders use it to verify information about you, see your borrowing activity and find out about your repayment history. Some of the information on your credit report is used to determine your credit score.

What is a Credit Score?

Your credit score is a number, based on specific information on your credit report. Your credit score is used by lenders to predict the likelihood that you will repay future debt. Your credit score changes frequently and it is up to each lender how they interpret and use your credit score.

What Does a Credit Score Mean?

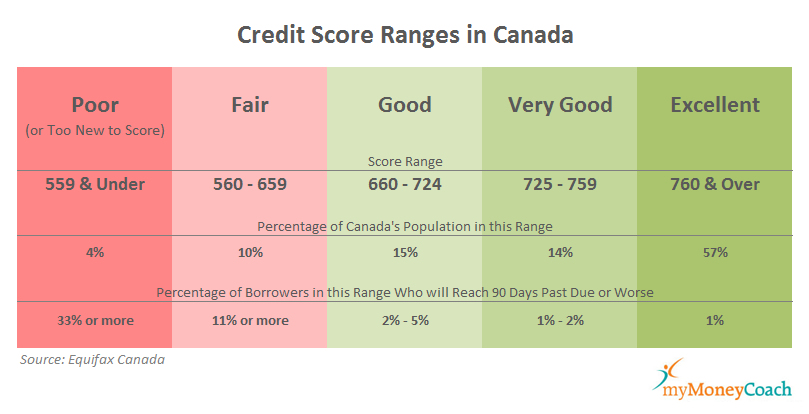

A credit score is a number which can range from a low near 300 to a high of 850 or 900 (depending on which company is calculating the score).

If someone’s score is 580, it means that “580 people out of 850 are likely to repay their debt.” If someone’s score is 780, it means that “780 people out of 850 are likely to repay their debt.”

The number represents the odds that a lender will get the money back that they lend someone. The higher the number, the better the odds.

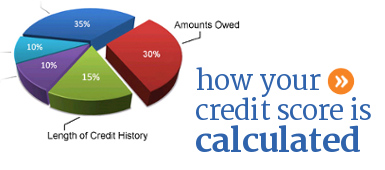

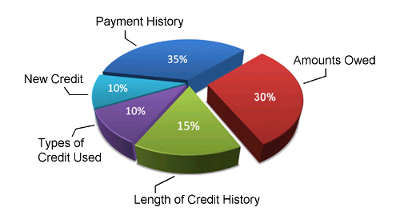

5 Key Factors in Calculating and Determining Your Credit Score

A number of specific factors go into determining a credit score. These factors are based on what someone does or doesn’t do with the credit they already have available. That is why the score changes frequently. Here are the 5 factors that determine your credit score:

1. Payment History (35%)

Your payment history is the most important factor in your credit score. Creditors want to know if you are going to pay them back the money you are asking to borrow from them.

Your payment history reflects all the payments you make to all of your consumer debts. Creditors report every time you make a payment to your credit cards, line of credit, car loan, personal loan, student loan, cell phone on contract and any other regular debts you have. Mortgage payments are not reflected on a credit report, but almost everything else is.

The payment information that is reported shows separately for each account you have. It shows whether or not you’ve paid as agreed, it shows if it is a deferred payment plan or if payments aren’t currently required (like for a student loan), how many past due payments you have, how often your payments have been late, if you have any debts in collections and if you have any negative information in the public records portion of your credit report (bankruptcy, judgments, liens, etc.).

Your score also reflects how recent any late payments or collection activities are. The older the information gets, the less it will impact your score.

2. How Much is Owed (30%)

When you apply for credit, how much you already owe really matters to a lender. Your current payments will determine if you can manage any more payments in your budget for the additional money you borrow.

While you might think that you can handle more credit, statistically speaking, there’s a chance you might not be able to. If you are close to maxing out all of your credit cards or your line of credit, it means that you are a higher risk to lenders. Higher risk to a lender means that there’s a greater chance that you won’t keep up with your payments.

Another aspect of this part of your credit score reflects how much of your available credit limits you use on an ongoing basis. If you usually use 60% or more of your credit limit on a credit card or line of credit, it will impact your credit score negatively. This is because if something were to happen to your income and you owe a lot of money, you would find yourself struggling to keep up with payments.

3. Length of Credit History (15%)

If you have had credit available to you for a long time, your credit report should provide an accurate picture of how you use credit and if you had one, how you got through a difficult time. For someone who has not used credit for very long time, it is difficult to tell if they really know how to use credit responsibly.

Good or bad, most information will be automatically removed from someone’s credit report after 6 – 7 years, so the only way to keep a credit report active, is to use credit, at least very minimally, on an ongoing basis.

Time is needed to get a true picture of how responsible someone is with credit. This is why the length of your credit history is the third most important factor in your credit score calculation.

Your score will reflect how long it has been since you first obtained credit, how long each item on your credit report has been reporting and whether or not you are actively using credit right now.

If you have recently obtained credit for the first time, your credit score will not be very strong. However, if you have been using credit responsibly for many years, this factor can work in your favour.

If you have been involved in a bankruptcy, consumer proposal, orderly payment of debt or debt management program, your credit history will essentially restart whenever you complete your program.

4. New Credit Applications (10%)

Frequently applying for new credit can signal financial difficulty. In the industry it’s called “credit shopping” and it does not reflect favourably on someone’s credit score.

It is not unreasonable for a creditor to worry about how often someone applies for new/more credit because the more new credit someone gets, the harder it becomes for them to keep up with all of their payments.

This part of your credit score takes into account the number of times your credit has been checked in the last 5 years, the number of credit accounts you have recently opened, how much time has passed since you opened any new accounts and the time since your most recent credit inquiries. This part of your credit score will also evaluate whether or not you are re-establishing your credit history following past payment problems.

5. Types of Credit Used (10%)

Even though this part of your credit score makes up 10% of the total, it is the least significant part, unless you don’t have much other information on your credit report.

Different types of credit shed light on how you handle your money overall. For example, deferred interest or payment plans can indicate that you aren’t able to save up for purchases ahead of time. Consolidation loans mean that you’ve had difficulty paying your debts in the past. A line of credit is a revolving form of credit, like a credit card, and it’s easier to get into trouble with a revolving form of credit than with an installment loan where you make payments for a set amount of years and then it’s paid in full.

If you focus on managing your finances wisely and only apply for credit as you need it, this part of your score should take care of itself.

Other Factors

The factors outlined above are calculated slightly differently by the two credit bureau companies in Canada, Equifax and TransUnion, and it is up to each lender to decide how they interpret and use credit scores and credit report information.

As such, the factors above are not the only things that are important when you apply for credit. Lenders will also consider factors such as your income, your assets, how long you have been at your job and the reason why you are applying for credit.

Is Knowing Your Own Credit Score Important?

Some people really want to know what their credit score is. However, it changes often, so be prepared. Also, keep in mind that your credit score is intended to reflect the likelihood that you will repay any money that you borrow. Most people don’t need a score to know if they will pay themselves back the money they lend themselves…. Instead, focus on managing your money carefully with a budget and only apply for credit that you need; your score will take care of itself.

Getting a copy of your credit report, however, is important and can be done for free. It will allow you to spot concerns, inaccuracies, or potential fraud.

If You Want to Get Your Credit Score

To find out what your credit score is, you can request it from Equifax and Trans Union, for a fee. If you don’t want to pay for it, you can try this credit score estimator to get a rough idea of what your credit score might be.

How to Improve Your Credit Score

The best things you can do to improve your credit score are to manage your money wisely using a realistic spending plan and to deal with your debts. Despite what some might claim, there is no quick-fix for factual but negative information on your credit report. Time and living within your means are what it takes to improve your credit rating. However, in some situations there may be a couple of things you can do to improve your score more quickly.

Related articles:

- Finding Solutions and Options to Deal with Debt

- Learn How to Build, Use and Re-Establish Credit

- 5 Steps to Re-Establish or Fix Your Credit in Canada

For more detailed information about credit reporting and what everything on a credit report printout means, take a look at this easy-to-read government resource, "Understanding Your Credit Report and Credit Score."